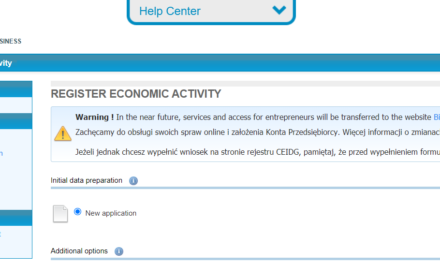

If you are B2B, Sole Trader Individual company then this post is for you. Until the 20th of February – this

Saturday – you can change your taxation for the financial year 2021. You can do that only once per year by the law. To do this, you must log in to the government website belonging to the City Hall,

responsible for the activities of entrepreneurs:

https://prod.ceidg.gov.pl/CEIDG/CEIDG.Public.UI/DecisionAdditionalParameters.aspx?type=2

After logging in with an E-puap trusted profile, select “change information” and under point no 18 select the new taxation. Once the tax is selected, click “Next” and sign the document again using the E-puap system.

Please see below some information about taxation options prepared by our partner Smartnumbers

| What form of PIT taxation should be chosen? |

| FORM OF TAXATION | GENERAL RULES – TAX SCALE | FLAT – RATE TAX | LUMP SUM ON REGISTERED INCOME | TAX CARD |

| TAX RATE | 17 % and after exceeding the income of 85,528 PLN the rate of 32% | 19% regardless of the income | from 2% to 17% depending on the type of conducted business activity Conditions: business activities from previous year had to be conducted individually income from business activities did not exceed 2 mln PLN | The rate specified in the amount for a given tax year is determined by the head of the competent tax office depending on the type and scope of conducted business activity, number of inhabitants in the place where the business activity is conducted, number of employees. |

| ADVENTAGES | the possibility of using tax benefits – tax-free amount – approximately PLN 8,000 per year, the right to settle accounts with the husband / wife, the right to settle accounts as a single parent, right to reduce revenues for tax deductible expenses incurred. | one tax rate, no limit on the amount of income you earn (with reaching 5 mln PLN per year, the obligation to establish LLC ), income from full time job does not sum and annual declaration fill separate: from activity or full time job. | fixed tax rate calculated on the amount of income | low and uniform tax value of the paid period, no obligation to use KPiR. |

| DISADVENTAGES | after exceeding the income of PLN 85,528, the entrepreneur is forced to pay income tax at 32% rates, income from all other jobs/income sum up. | no possibility of using tax benefits, no the right to settle accounts with the husband / wife, no the right to settle accounts as a single parent, no tax-free amount. | Difficulty in receiving the loan, No deduction of costs from income tax. | deductible costs cannot be deducted from revenues, the option to deduct only the health insurance contribution (7.75%), payment regardless of income achieved. |

(Visited 510 times, 1 visits today)